On Tuesday 8 May 2018, Treasurer Scott Morrison handed down his 3rd Budget. In what is widely perceived to be an election Budget, according to the Treasurer, the Budget is forecast to return to a modest surplus of $2.2 billion in 2019-20 (a year ahead of what was previously expected).

GPD is forecast to grow by 2.75% in 2017-18 and is forecast to accelerate further to 3% growth in 2018-19 and 2019-20, a pace the Government considers sufficient to continue to lower the unemployment rate over the next few years.

“Headline” items likely to be of interest to our business and investor clients are as follows:

Personal Taxation

Income Tax Rates

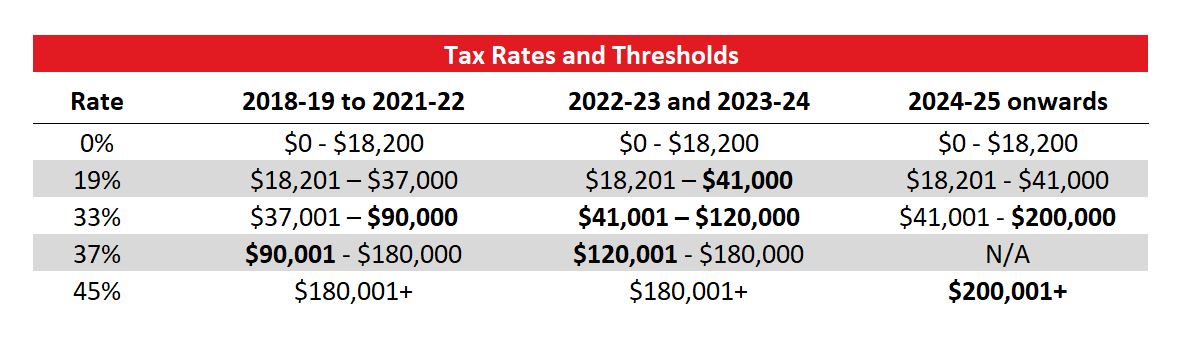

The Government is proposing a major 7-year 3-step plan to reform personal income tax. This will result in an increase in income levels at which higher rates of tax cut in and eventually a maximum rate of 32.5%, for those earning up to $200,000 p a. At that time, the Government estimates that only 6% of people will pay the top rate of 45%.

Tax rates and thresholds for 2018-19 onwards

The following table reflects the Government’s announced personal tax rate and threshold changes (highlighted in bold), excluding the 2% Medicare levy:

Minors and Testamentary Trusts: Concessional Tax Rates Limit

The concessional tax rates available for minors receiving income from testamentary trusts will be limited to income derived from assets that are transferred from deceased estates, or the proceeds of the disposal or investment of, those assets. Currently, income received by minors from testamentary trusts is taxed at normal adult rates rather than the higher tax rates that generally apply to minors.

The Government is concerned that some taxpayers are able to inappropriately obtain the benefit of this lower tax rate by injecting assets unrelated to the deceased estate into testamentary trusts. This measure will clarify that minors will be taxed at adult marginal tax rates only in relation to income of a testamentary trust that is generated from assets of a deceased estate (or the proceeds of the disposal or investment, of these assets).

This measure applies from 1 July 2019.

Business Taxation

$20,000 Instant Asset Write-Off for SBE's Extended by 12 Months

The Government will extend the current instant asset write-off ($20,000 threshold) for small business entities (SBE’s) by 12 months to 30 June 2019. This applies to businesses with aggregated annual turnover less than $10 million.

The threshold amount was due to return to $1,000 on 1 July 2018. As a result of this announcement, SBE’s will be able to immediately deduct purchases of eligible depreciating assets costing less than $20,000 each, that are acquired between 1 July 2017 and 30 June 2019 and first used or installed ready for use by 30 June 2019, for a taxable purpose.

Deductions Disallowed for Holding Vacant Land

The Government will disallow deductions for expenses associated with holding vacant land. Where the land is not genuinely held for the purpose of earning assessable income, expenses such as interest costs will be denied. The Government hopes this measure will reduce the tax incentives for “land banking”, which limit the use of land for housing or other development.

The measure will apply to both land held for residential and commercial purposes. However, the “carrying on a business” test would generally exclude land held for a commercial development. It will not apply to expenses associated with holding land that are incurred after:

- a property has been constructed on the land, it has received approval to be occupied and available to rent; or

- the land is being used by the owner to carry on a business, including a business of primary production.

Disallowed deductions will not be able to be carried forward for use in later income years. Expenses for which deductions will be denied could be included in the cost base if it would ordinarily be a cost base element (ie borrowing costs and council rates) for CGT purposes. However, if the denied deductions are for expenses which would not ordinarily be a cost base element, they cannot be included in the cost base.

This measure applies from 1 July 2019.

Superannuation

SMSF Member Limit to Increase From 4 to 6 - Law to be Amended

The Budget confirmed that the maximum number of allowable members in new and existing self-managed superannuation funds (SMSF’s) and small APRA funds will be expanded from 4 to 6 members, from 1 July 2019.

The proposed increase to the maximum number of SMSF members seeks to provide greater flexibility for large families to jointly manage retirement savings.

Super Guarantee Opt-Out for High-Income Employees Who Breach Concessional Cap

The Government will allow individuals whose income exceeds $263,157 and have multiple employers, to nominate that their wages from certain employers are not subject to the superannuation guarantee (SG), from 1 July 2018.

AS SG contributions are counted as concessional contributions, high-income earners with several employers (eg doctors who are employees of multiple hospitals and company directors holding a number of board positions) are especially at risk of inadvertently breaching the annual concessional cap of $25,000.

The measure will allow eligible individuals to avoid unintentionally breaching the $25,000 concessional cap as a result of multiple compulsory SG contributions.

Employees who use this measure will be able to negotiate to receive additional income (which is taxed at marginal tax rates), instead of SG contributions.

SMSF Audit Cycle of 3 Years for Funds with Good Compliance History

The annual audit requirement for self-managed superannuation funds (SMSF’s) will be extended to a 3-yearly cycle, for funds with a history of good record-keeping and compliance.

The measure will apply to SMSF trustees that have a history of 3 consecutive years of clear audit reports and that have lodged the fund’s annual returns in a timely manner.

This measure will start on 1 July 2019.

SMSF Trustees Required to Formulate Retirement Income Strategy for Members

The Superannuation Industry (Supervision) Act 1993 (SIS Act) will be amended to introduce a retirement covenant that will require superannuation trustees to formulate a retirement income strategy for fund members. This requirement appears to be aimed at supporting the Government’s proposed development of a comprehensive income product for retirement (CIPR) framework.

Currently the SIS Act includes covenants requiring trustees to formulate, review regularly and give effect to, an investment strategy and an insurance strategy.

The start date for this new retirement income strategy requirement was not stated.

Should you have any queries in relation to the Budget please do not hesitate to contact us via our website, or call us on +61 3 9840 2200.