On Tuesday 12th May 2026 Treasurer, Jim Chalmers, handed down the Federal Budget 2026-27, noting it to be "the most important and ambitious budget in decades".

Measures designed to deliver intergenerational equity will see an overhaul of negative gearing and the capital gains tax discount plus a 30% tax on discretionary trust distributions.

Small businesses will see the permanent extension of the $20,000 instant asset write-off and the reintroduction of ‘loss carry back’ for companies.

A new $250 tax offset for working Australians will run alongside an instant tax deduction for work-related expenses plus the already announced tax cuts will help individuals.

Budget Highlights

Individuals

- A $250 ‘Working Australian’s’ tax offset will be introduced from 1 July 2027

- $1,000 instant tax deduction starting from the 2027 financial year

- Taxpayers will be allowed to claim this tax deduction without the need to keep receipts to support this claim (no substantiation necessary)

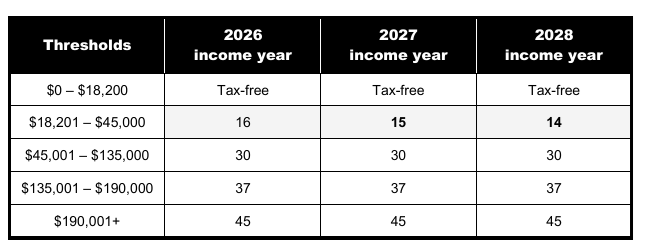

- Tax cuts – marginal tax rate cuts will lower the average tax rate from 25.5% to 24.7% by FY28

Business

- Companies will be allowed to carry back tax losses for up to two years

- For tax years commencing on or after 1 July 2026, companies with aggregated annual global turnover of less than $1 billion will be able to carry back a tax loss and offset it against tax paid up to two years earlier. Loss carry back will apply to revenue losses only and will be limited to a company’s franking account balance.

- Permanent extension of the $20,000 instant asset write-off for small businesses with turnover of less than $10 million

Negative Gearing Reform

From 1 July 2027, the government will limit negative gearing for residential property investment to new builds.

- Existing investment properties can still be negatively geared until sold

- Properties purchased between 12 May 2026 and 30 June 2027 can only be negatively geared until 30 June 2027

- Properties purchased after 1 July 2027 will not be allowed to be negatively geared (apart from new builds)

- However, losses made from investment properties can be carried forward to offset future rental income in later years

Capital Gains Tax Reform

From 1 July 2027 the 50% general discount will be replaced for individuals, trusts and partnerships with cost base indexation and a 30% minimum tax rate on capital gains

- Indexation will be calculated using CPI in a similar manner to arrangements previously in place between 1985 to 1999.

- The ATO will provide further guidance and tools to support calculation of this adjustment

- These changes will apply to all CGT Assets

- Minimum tax of 30% to apply to all capital gains, regardless of marginal rate

- Pre CGT assets will also be taxable from 1 July 2027

- Transitional rules for Capital Gains Tax assets

- For investments apart from property, no changes for assets purchased or sold prior to 1 July 2027.

- Assets purchased after 1 July 2027 will be wholly treated under new arrangements

- For assets owned prior to 1 July 2027 and sold after 1 July 2027 will be treated under current arrangements on gains made prior to this date, and under new arrangements for gains made after this date.

- The 50 per cent CGT discount will apply to the difference between the asset’s cost base and its value at 1 July 2027. Indexation and the minimum tax will be used to calculate the CGT on gains accruing from 1 July 2027 (using the asset’s value at 1 July 2027 as the asset’s cost base).

Taxation of discretionary trusts

Discretionary Trusts will have a minimum tax of 30% imposed on them from 1 July 2028.

- Tax to be paid by the trustee, which will flow to the beneficiaries as a non-refundable tax offset

- This minimum tax will only effect discretionary trusts – not fixed trusts, deceased estates or superfunds

Reducing the FBT concession for electric vehicles

From 1 April 2029, a permanent 25% discount on FBT will be available for all electric cars valued up to and including the fuel-efficient luxury car tax threshold, implemented through a 15% rate in the statutory formula. The following transitional arrangements will apply:

- All eligible electric cars will retain the FBT discount rate that was in place when the arrangement commenced.

- All electric cars valued up to and including $75,000 that are provided before 1 April 2029 will continue to be eligible for a 100% discount on FBT, implemented through a 0% rate in the statutory formula.

- Electric cars valued above $75,000 and up to and including the fuel-efficient luxury car tax threshold that are provided between 1 April 2027 and 1 April 2029 will be eligible for a 25% discount on FBT, implemented through a 15% rate in the FBT statutory formula.

The existing 20% statutory rate will continue to apply for all other cars, including electric cars costing more than the fuel-efficient luxury car tax threshold.

Reportable fringe benefits will continue to be determined for eligible electric cars as if a 20% FBT statutory formula rate or cost basis method applied.

Planning will be key

Aside from the tax cuts previously announced, these changes are not yet legislated. Planning ahead will be important in navigating any potential impact.

As always, our team is here to guide and support you. If you are concerned about the impact of the budget announcements on you, your family or business please contact us for advice or reassurance.

Further Resources

For more information, read these supporting guides from the Budget website.

Tax Explainer - New tax cuts for Australian workers

Tax Explainer - Negative Gearing and Capital Gains Tax Reform